Why is it Difficult to Save Money?

Everyone finds it difficult to either spend or save money. For most of us, the struggle is with saving! In fact, 70% of people have less than $1,000 for an emergency fund. Of course, we all know that saving money is important, so why does it feel impossible for so many people?

Most of the time, problems with saving money have nothing to do with financial literacy or maturity. Put down that shame, friends, that’s not what this is about! Today, I want to talk to you about some of the real reasons people struggle to save money. Hopefully, you can find your own money-saving hurdle and clear it with a little guidance. :)

Here is why it’s difficult to save money:

Why is it Difficult to Save Money?

Too Much Debt

If you have a lot of debt, saving money can be very hard. The high minimum payments combined with the high-interest rates push many to live paycheck-to-paycheck. Debt adds so many payments to your monthly expense list, that you often feel like you’re drowning!

Most people (and most of my clients) carry student loan debt, car loan debt, personal loan debt, medical debt, and credit card debt. In fact, the average American has $21,800 in personal debt (not including the house.) The average monthly car payment in the U.S. is over $700. The average credit card payment is $430. The average student loan payment is $284. With interest, these minimum payments barely move the mark toward paying off the debt principal.

Paying on all this debt can be so overwhelming, that many struggle even if they have a good income. High debt-to-income ratio can still have you scrambling to pay the bills, even when you have a sizable salary. Your debt is stealing the opportunities your income provides, so focusing first on paying off debt, before tackling big savings goals, is going to be your best plan!*

*However, I highly recommend having a $1,000 emergency fund savings before tackling your debt.

Overspending on Nonessentials

There are monthly expenses that are essential. You can’t avoid buying groceries, paying the gas bill, and sending a check to your daycare provider. However, if you’re struggling to save, it could be because you’re spending a lot on things that are not essential.

Grabbing a Starbucks coffee a few times a week or picking up home decor at Target from time to time may not seem like a big deal, but it can definitely add up. Just think, the average price of a venti Starbucks beverage is $3.25. If you get that 15 times in a month, that’s nearly $50! $50 a month could turn into $600 in savings after a year. And, that’s just cutting one nonessential expense!

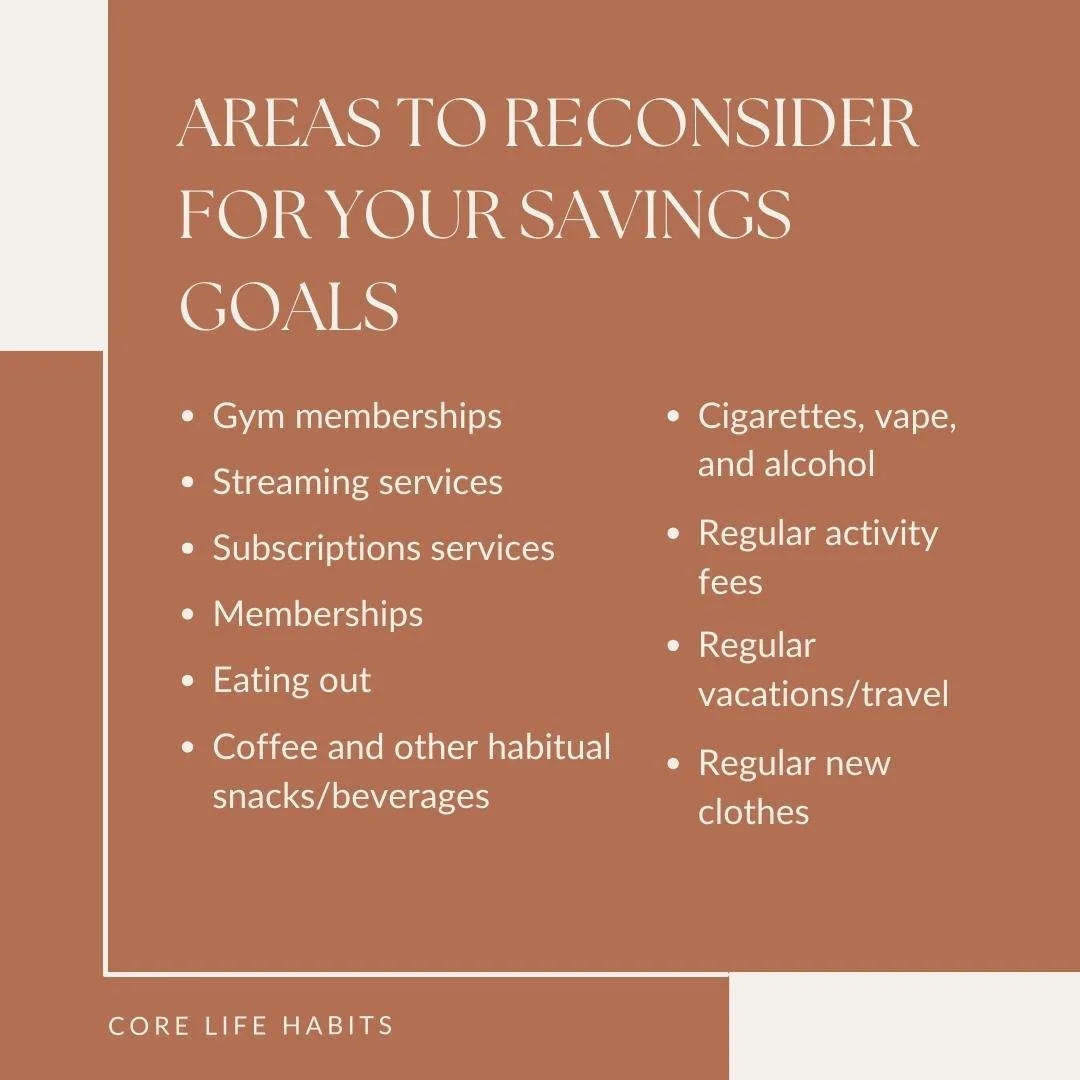

As a financial coach, I help people sift through their expenses and have them track ALL of their spending to see where potential savings could be made. We don’t cut everything fun, of course, but here are some areas you could reconsider, at least until you reach your savings goals:

Gym memberships

Streaming services

Subscriptions services

Memberships

Eating out

Coffee and other habitual snacks/beverages

Cigarettes, vape, and alcohol

Regular activity fees

Regular vacations/travel

Regular new clothes

These expenses saved could add up to a pretty big emergency fund! Don’t underestimate the power of slashing nonessential costs!

Lack of Intentional Budgeting

Budgeting is the key to getting control of your money. A budget doesn’t just document what you spend after the fact, it’s you planning your spending before it even happens. When you use a budget to plan your spending, you don’t look at your bank account at the end of the month and think, “Where did all my money go?” You’ll know exactly where all your money went. To all the places you told it to go, of course! :)

The type of budgeting I recommend is called “zero-based” budgeting. It’s where every dollar has an assignment, which means zero opportunity for overspending. Your budget manages all your monthly spending and savings, so there’s no room for surprises or mistakes. Follow your budget plan and you’ll reach your savings goals! Of course, “just follow the plan” can be easier said than done. If you feel this way, we should chat! Click here to book some time with me. :)

Not Tracking Your Spending

Budgeting is an proactive process, not reactive. It’s not just about making fresh spending plans every month, it’s about following it through every time. When you’re tracking how you’re spending money, it’s pretty easy to identify when you’re about to overspend in a category or where you might have a little extra. That way, you can adjust your plan and keep yourself accountable to stay on track and save money! Almost every one of my clients who leave coaching tell me how much more aware they feel about where their money is going and in turn have more confidence about how to handle it. They all attribute it entirely to tracking their spending!

Low Income

You may feel like you’re pretty disciplined and yet you still can’t grow your savings. This may be because you don’t make enough to cover your living expenses and savings plans. If your entire income goes to necessities and there’s only a hundred dollars or so left every month, building savings is going to be really difficult. If this is you, it may be time to consider increasing your income with a new job, a second job or side gigs. (I know, easier said than done, but you can do it!)

Savings is Not Set to Auto-Draft

If you’re a spender, transferring money into your savings account can feel like pulling teeth. There’s always a tempting product or service to spend the extra cash on instead, and chances are you’ll prioritize that thing over moving extra cash into your savings account.

This is why it’s always a good idea to set up your bank account to auto-draft your monthly savings amount from your checking account to your savings account. When you do this, your savings transfer happens like any other bill withdrawal. This will help shift your mindset and make saving a priority like paying your phone bill!

Plus, when you set it and forget it, you truly forget it. Hopefully, before you know it, that savings account will be full and you didn’t do anything crazy to get there—you just followed your budget and let the auto-draft do its thing!

Unestablished Future Goals

Pushing yourself to save (whether it’s for an emergency fund or Christmas presents) is all about drive. The truth is, it’s hard for a lot of us to put things in savings because we want instant satisfaction. Delaying satisfaction through savings is hard, and it’s even harder without the right motivation. What are you saving for? What will the savings do for you?

Lack of established financial goals is another big reason I see clients struggle to save money. They don’t really know why they’re saving other than it’s “what they’re supposed to do.” They haven’t taken time to envision and plan what their life would look like with a strong emergency fund and money in the bank for big expenses. So, take some time to write down your future money goals and how a savings plan will help get you there.

For more on vision planning, read my post about common reasons people fail at their goals. (It’ll help you avoid common goal-setting mistakes!)

No Accountability

Saving doesn’t come naturally to many of us and you shouldn’t beat yourself up about it. Some people really struggle to workout regularly, eat healthy, or clean their house, even! It’s a LOT to maintain a household, ourselves, work, kids, all of it. That’s why personal trainers, nutritionists, and house cleaners exist! To help keep them on track. At the end of the day, we all need help in different areas of our lives. And that’s okay!

If you feel like you lack discipline or strength in an area of your life, accountability is key. You can get accountability sometimes through a friend or family member, but a trusted coach is the best way to go. They have the right expertise to guide you through every step of your financial journey, and they’ll give you the tools to change your habits. The great thing about a coach in this space is that they’re completely disconnected from your immediate network. Taking financial advice from a family member or friend isn’t necessarily wrong, but not always the best option. As a certified financial coach, I can help keep you accountable, help you establish your future goals, learn strong money management skills, and, most of all, save big!

Saving money is hard, but these tips can help you reach your goals!

I hope this post helped you understand why saving money can be difficult. Remember, you’re not alone! If you’ve tried and tried again, but you feel like you’re not seeing the results you want on your own, try these tips and consider financial coaching! Together, we can vision plan, pay off your debt, and start saving like you’ve always wanted. Until then, browse the blog for more financial tips and life advice! See you next week!